Is Revolut becoming the ‘Amazon’ of banking?

Introduction

What if you could have your bank at your fingertips? It could seem fictional decades ago, mainly because of the overestimated customers’ willingness to switch away from traditional banks and the underestimated high costs of customer acquisitions (Anon, 2018). Yet, the financial landscape has drastically changed now. Due to the rapidly evolving financial demands of millennials, emerging competitors, and changing regulations, there has been an accelerated shift to digital banking (Shalvey, 2019).

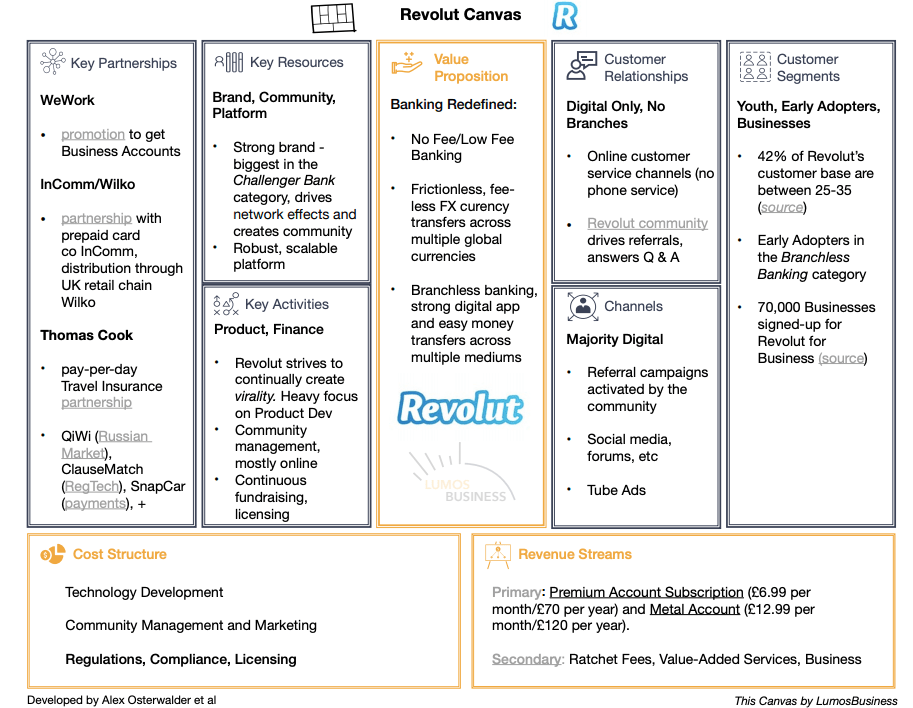

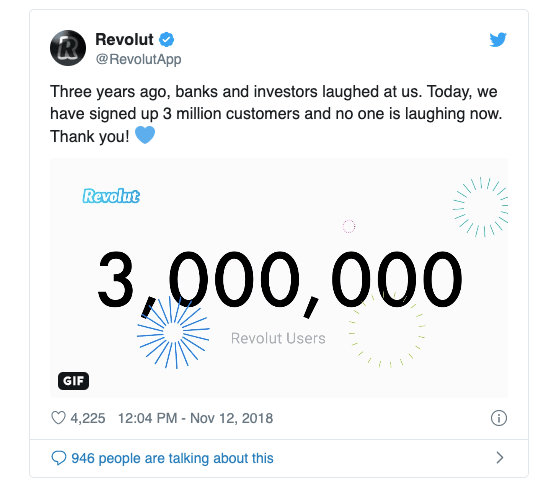

Revolut, a UK based fintech launched in 2015, has been one of the major players to challenge the banking convention. Leveraging on its digital business model to offer clients cheaper, convenient and more transparent services, it has amassed over seven million regular users in over 29 countries, 100,000 business customers, and has facilitated £40bn worth of transactions as of 2019 (Williams, 2019).

But how has Revolut’s digital business model contributed to its success?

Freemium business model

Revolut adopted a freemium business model by offering free basic accounts, which offers currency exchange at live conversion rates, following which the Fintech company gained massive customer adoption (Anon, 2018). It earns its revenue by monetising its users on several levers, including premium services for both consumers and businesses (Bhattacharyya, 2018). Moreover, by eliminating the middleman in the business model and building its infrastructure in-house, it has been able to provide competitive pricing (Browne, 2019). The successful business model empowered Revolut to grow its market share with a lower fixed cost, which led to its first profit in December 2017- the first of any digital banking start-up (Anon, 2018).

However, arguably the freemium business model comes with a hidden cost to the customers. There have been raising concerns around how Revolut is monetizing on users’ data. According to Revolut, data collected may be sent to credit bureaus, social media companies and analytics firms. It also collects location and usage data to send users relevant advertisements and to track users’ nearby contacts (Short, 2019). This issue raises an essential question, to what extent will companies such as Revolut exploit user’s data in the search for more profits?

Zero Marketing – Community Virality

Another success factor of Revolut’s digital business model is its strategy to keep customers engaged in its ecosystem. The approach is to generate community referrals and product virality (Bhattacharyya, 2018). The logic being that if Revolut solves the everyday problem of its community, they are most likely to recommend Revolut to their networks (Braileanu, 2017). As a result, in 2018, the FinTech company was able to have 100,000 customers in their waiting list in the U.S without any marketing (Schulze, 2018). The community-first brand has helped Revolut to retain its loyal users and eventually grow its user-base (Finningley, 2019).

The community virality is one of Revolut’s expansion strategy to become a global bank. However, it has faced concerns based on legitimacy and compliance with national and international regulations (Cook, 2019). Financial services are one of the most regulated industries in the world, wherein different jurisdictions often apply distinctive measures in regard to tax, labour and data (Jefferies, 2017). Revolut tackled this by acquiring E-money licences, whereby it has been able to effectively attract a lot of customers and spend twice less than its competitors (PWC, 2020). However, with Revolut’s global ambition, it might struggle to deal with the regulatory frameworks that authorities have set up in different jurisdictions.

Building a platform fit for the digital age

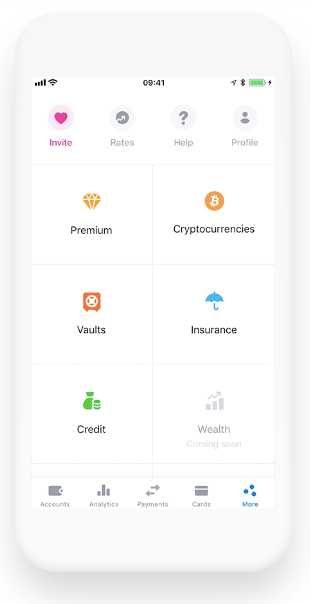

Revolut’s selling point was its transformation of the slow and clunky banking platforms to a platform with design, functionality and speed at its core (Braileanu, 2017). Revolut’s strategy completely rejects the marketplace banking model. It seeks to build a multi-product platform to become ‘one of the biggest financial services companies in the world’, with a full offering, including business lending, retail lending, trading, investments, and wealth management (Anon, 2018). To support its goal, Revolut has been investing in promising technology including Blockchain, Cloud Technology and Artificial Intelligence. Mainly, Sherlock, a machine learning-based fraud prevention system that continuously and autonomously monitors all Revolut’s users’ transactions has been significant innovation in the Fintech market (Lewis, 2017).

However, the experimentation of these new technologies has sparked some controversy. Last year, the company’s new automated compliance system failed to block thousands of potentially suspicious transactions on its platform for three months. It was followed by a report by FCA and National Crime Agency that warned the digital bank of suspected money laundering in its app (Cook, 2019). This issue raises the question of how should fintech be regulated to address these risks and concerns?

Conclusion

Revolut’s profitability, the scale of customer uptake and technological innovation is proof of its successful and resilient digital business model. Just like users enjoy the experience of using apps such as Uber, Netflix, Instagram, banking customers deserve a seamless banking experience. Revolut aims to be one app with tens of millions of users, where they can manage every aspect of their financial life with the best value and technology (Aldalou, 2018). What do you think will take Revolut to achieve its goal?

_ . _ . _ ._ . _ . _ ._ . _ . _ ._ . _ . _ ._ . _ . _ ._ . _ . _ ._ . _ . _ ._ . _ . _ ._ . _ . _ ._ . _ . _ ._

References

Aldalou, M. (2018). Revolut takes leap towards becoming ‘Amazon of Banking’. Retrieved 6 March 2020, from https://www.businesscloud.co.uk/news/revolut-takes-leap-towards-becoming-amazon-of-banking

Anon. (2018). Revolut Strategy Teardown. Retrieved 6 March 2020, from https://redesigning-fs.com/wp-content/uploads/2018/11/Revolut-strategy-teardown-by-RFS.pdf

BHATTACHARYYA, S. (2018). Inside UK startup bank Revolut’s revenue model – Tearsheet. Retrieved 6 March 2020, from https://tearsheet.co/modern-banking-experience/inside-uk-startup-bank-revoluts-revenue-model/

Braileanu, R. (2017). How Revolut signed-up 16,000 business accounts in 3 months. Retrieved 6 March 2020, from https://blog.revolut.com/how-revolut-signed-up-16-000-business-accounts-in-3-months-with-no-marketing/

Browne, R. (2019). Inside Revolut’s bid to be the Amazon of banking, and the lessons it’s learned from breakneck growth. Retrieved 6 March 2020, from https://www.cnbc.com/2019/07/05/revolut-ceo-nikolay-storonsky-on-the-fintech-unicorns-journey.html

Cook, J. (2019). Digital bank Revolut’s sanctions screening issue revealed. Retrieved 6 March 2020, from https://www.telegraph.co.uk/technology/2019/02/28/revolut-failed-block-suspicious-transactions/

Cook, J. (2019). Inside Revolut and why the booming finance firm is facing a tide of criticism. Retrieved 6 March 2020, from https://www.telegraph.co.uk/technology/2019/05/05/made-mistakes-past-inside-revoluts-rocky-start-biggest-year/

Finningley, J. (2019). Business Model Canvas – Revolut. Retrieved 6 March 2020, from http://lumosbusiness.com/business-model-canvas-revolut/

Jefferies, G. (2017). Internationalisation of FinTech: What Barriers do FinTechs Face Compared to Incumbents and How Can They Be Effectively Overcome? – Innovate Finance – The Voice of Global FinTech. Retrieved 6 March 2020, from https://www.innovatefinance.com/money-talks-live-event/internationalisation-fintech-barriers-fintechs-face-compared-incumbents-can-effectively-overcome/

Lewis. (2017). How Revolut are leading the way with cryptocurrencies. Retrieved 6 March 2020, from https://blog.revolut.com/how-revolut-are-leading-the-way-with-cryptocurrencies/

PWC. (2020). Financial Services Technology 2020 and Beyond: Embracing disruption. Retrieved 6 March 2020, from https://www.pwc.com/gx/en/financial-services/assets/pdf/technology2020-and-beyond.pdf

Schulze, E. (2018). UK fintech unicorn Revolut granted European banking license. Retrieved 6 March 2020, from https://www.cnbc.com/2018/12/13/revolut-secures-european-banking-license.html

Shalvey, K. (2019). Banks of 2030 will be in the ‘palm of your hand,’ PwC associate director says. Retrieved 6 March 2020, from https://www.cnbc.com/2019/11/19/pwcs-gazmararian-banks-of-next-decade-will-be-in-palm-of-your-hand.html

Short, E. (2019). Why Revolut is going to start sharing your data with credit bureaus. Retrieved 6 March 2020, from https://www.siliconrepublic.com/enterprise/revolut-privacy-policy-credit-bureaus-targeted-advertising

Williams, H. (2019). Revolut Business review | Try Revolut for Business | Startups.co.uk. Retrieved 6 March 2020, from https://startups.co.uk/revolut-business-account-review/

Follow My Blog

Get new content delivered directly to your inbox.

Great job, Antish.

I’m particularly interested in what you said about Revolut falling afoul of FCA and NCA regulations because it failed to investigate or block suspicious transactions made through the app. To me, this raises the question of whether we can trust fully-automated technology with something as important as our money; it seems, at least for the moment, that technology has not advanced to the extent that technical errors can be reliably circumnavigated. In light of this, is it sensible for us to place our faith in a system like the one Revolut employs?

The article below (from Panda Security) asks whether we perhaps place too much trust in our technology. The article touches on the illusion of privacy we are constantly fed by social media and banking sites (amongst others) and the ubiquity of security breaches that result in people’s personal and banking information being exposed. It finishes by encouraging us to ‘take a default position of mistrust’ to avoid important information falling into the wrong hands. This would obviously lead one to be skeptical of apps like Revolut that are asking us to place even more trust in the capacity of digital technology to provide total security. Do you agree with this perspective?

Felix

LikeLike

Forgot to add the link, here it is:

https://www.pandasecurity.com/mediacenter/security/trust-privacy-technology/

LikeLike

Hi Antish, it is an excellent discussion about Revolut. Your blog present the way which digital business model contributed to Revolut’s success, and potential problems or challenges from 3 dimensions with clear structure.

It is notice that almost all digital company will adopt freemium and platform those two digital business patterns. I am interested in “community virality”, which is a kind of word-of-mouth advertising? Could you explain it more specifically?

Currently, More and more traditional banks have their own online platforms, which is no different from Revolut. What’s more, they are more reliable and secure. In that case, what Revolut can do?

There already been some very mature cloud computing technology developed by Amazon, Microsoft, Google and IBM. Should it use existing cloud computing technology (like AWS) or develop on its own? In my view, instead of investing this technology, they should pay attention to other areas.

LikeLike

Hello Antish

You did a great synthesis work. You successfully pointed out on two important challenges Revolut is facing, both the regulatory environment that may block further expansion, this last problem seems to be relative; it did not prevent the company to raise and its relative technical unreliability when it comes to manage a digital platform.

On this last issue, it seems that Revolut is facing a structural problem. One may point out its tendency to blame its third-party service providers, especially payment processor. Those processes would need to be internalize but still have not.

Moreover, my question would be how sustainable do you think is the digital business model of Revolut? In addition with those internal weaknesses and although they still managed to get funds with 500 million dollars raised at the end of 2019, the firm remains still loss making.

References:

Kelly, J., 2019. Revolut’S Growing Pains Rumble On. [online] Financial Times. Available at: [Accessed 11 March 2020].

Thomson, A., 2020. Bloomberg – Are You A Robot?. [online] Bloomberg.com. Available at: [Accessed 11 March 2020].

LikeLike

Hi Antish! A thought-provoking and well researched article. It reminded me of the topic of your previous article, about the value of developing products that are not necessarily ‘perfect’ in their initial stages, but give businesses a competitive edge by being ‘first movers’ within the market. In response to your question, ‘to what extent will companies such as Revolut exploit users’ data in the search for more profits?’, I think it is definitely a business model component that will increasingly contribute to company profit. This article -https://www.wired.com/story/should-big-tech-own-our-personal-data/- includes an interesting point from a European competition commissioner, Margrethe Vestager, who argued, for example, that she would ‘like to have a Facebook in which I pay a fee each month, but I would have no tracking and advertising and the full benefits of privacy’. As users tire of the downsides of Freemium, I believe it will either turn them away completely from a product, or invest more money into Premium. What do you think?

LikeLike

Antish,

A timely piece of an article just when Revolut has been announced as the UK’s most valuable fintech startup. Revolut’s freemium business model has indeed attracted the millennials to adopt digital banking, which has less bureaucracy than traditional banking. However, I agree with the data security issue as recent missteps of asking applicants to secure new customers for free in order to have a chance at getting a job without full disclosure raised concern on its customer onboarding process. Also, in this era of intense competition with other fintech like Monzo and Monesa, Revolut has failed to incorporate a few unique features. For example, Revolut only allows direct debits from the accounts in the euro, and people cannot use it to pay in sterling directly. While its competitors instead support this function. Do you think Revolut should be more competitive to win a share of the digital-business pie?

Sources:

Makortoff, K. (2019). Digital bank Revolut becomes UK’s most valuable fintech startup. Retrieved 11 March 2020, from https://www.theguardian.com/business/2020/feb/25/digital-bank-revolut-becomes-uk-most-valuable-fintech-startup-cash-injection-airbnb-spotify

Mellino, E. (2019). Revolut says it’s cleaning up its act. Evidence suggests otherwise. Retrieved 11 March 2020, from https://www.wired.co.uk/article/revolut-compliance-free-work-fintech-application-toxic-storonsky

Barton, C. (2019). Revolut vs Monzo | Which comes out on top?. Retrieved 11 March 2020, from https://www.finder.com/uk/revolut-vs-monzo

LikeLike